The trade composition of GCC countries can be as described as highly asymmetrical with exports concentrated largely in crude oil while imports are diversified. This makes the economies vulnerable to fluctuations in international commodity market – oil in particular. The GCC are amongst the most open in the world with no foreign exchange controls and low tariff and quota protection.

GCC countries as is evident are export led economies with over 50% of GDP exported. Fuel exports form almost 85% of total exports for Saudi Arabia and Oman, 95% for Kuwait and 88% for Qatar. Based on factor endowments, the Saudi economy is primarily an oil economy and is the largest exporter of crude oil in the world.

Thus, while Saudi exports are predominantly oil oriented, one finds that over time non-oil exports increased with the ongoing diversification of the economy. Its main export partners are China, Japan, USA, India and South Korea.

Due to lack of water, GCC countries import more than one third of their food requirements. Major imports of Saudi Arabia are food items, machinery and equipment, vehicles and textiles. The net exports are positive for all GCC countries which indicate healthy foreign trade balance but the same is driven highly by oil prices. As oil prices become more stable and oil reserves deplete, this balance may get disturbed causing B o P problems in future years if diversification is not enough.

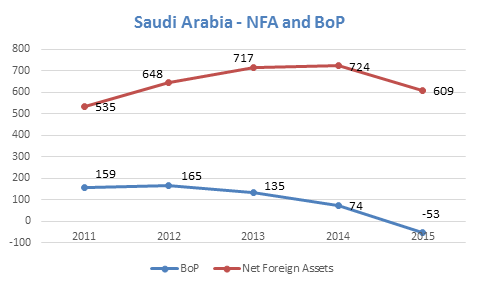

The balance of payments of Saudi Arabia warrants attention. Following many years of large surpluses, the current account shifted into a sizeable deficit in 2015. This reflected the slump in oil earnings, allied to only a very mild adjustment in import spending.